Most businesses turn to invoice factoring for cash flow, but did you know that it can actually improve key financial ratios and strengthen your company from the inside out? In this detailed factoring guide, we’ll explore the link between factoring and financial ratios that matter, why the shift occurs, and what to look for.

How Factoring Services Work

Factoring is a way to turn your outstanding B2B invoices into immediate working capital. It is not a loan. You’re selling your receivables at a slight discount to a third party called a factoring company. An example of how it usually works in practice is outlined below.

- You Issue an Invoice to Your Customer: Standard terms apply, such as Net 30 or Net 60.

- You Send a Copy of the Invoice to the Factoring Company: They verify the invoice and the creditworthiness of your customer.

- You Receive an Advance: A typical advance rate is between 80 and 95 percent of the invoice amount and is deposited into your account within one or two business days.

- Your Customer Pays the Factoring Company: Payment is made based on the original terms.

- You Receive the Remaining Balance: Once the invoice is paid in full, the remaining amount is sent to you, minus the factoring fee.

Another major distinction between factoring and traditional financing is that approval is based on the quality of your receivables, not your credit score, collateral, or time in business.

It’s used by businesses in transportation, manufacturing, staffing, and other B2B industries where delayed payment terms are standard and cash flow gaps are common. Some use it as a short-term solution. Others rely on it as part of a long-term working capital strategy.

Overview of Financial Ratios and Their Role in Business Evaluation

The importance of financial ratios for SMEs cannot be overstated. They’re essential tools for evaluating the stability, efficiency, and overall performance of a business. They transform raw figures from your financial statements into benchmarks that can guide internal decisions and shape how others perceive your company.

Knowing how to interpret key ratios allows you to monitor trends, identify potential issues early, and make more informed financial decisions. These same ratios are also used by external stakeholders, such as banks, investors, and factoring companies, to assess your business’s financial health. Strong ratios can help establish credibility and support access to funding. Weak or inconsistent ratios may raise concerns or delay approvals.

Common Sources and Calculation

Most ratios are calculated using figures from your balance sheet and income statement. Accounting platforms such as Xero, FreshBooks, and QuickBooks often include built-in ratio reporting, which can streamline the process. But even when the math is automated, understanding the results is what makes them useful.

Core Categories of Financial Ratios

Financial ratios are generally organized into three categories: liquidity, debt, and profitability.

- Liquidity Ratios: Assess your business’s ability to meet short-term financial obligations.

- Debt Ratios: Evaluate how much leverage your business is using and how reliant it is on external financing.

- Profitability Ratios: Measure how efficiently your business is turning revenue into profit.

Each category provides a different perspective. Together, they offer a well-rounded view of your financial position. In the sections that follow, we will explore how factoring impacts liquidity, debt, and profitability ratios, and what that means for your business over time.

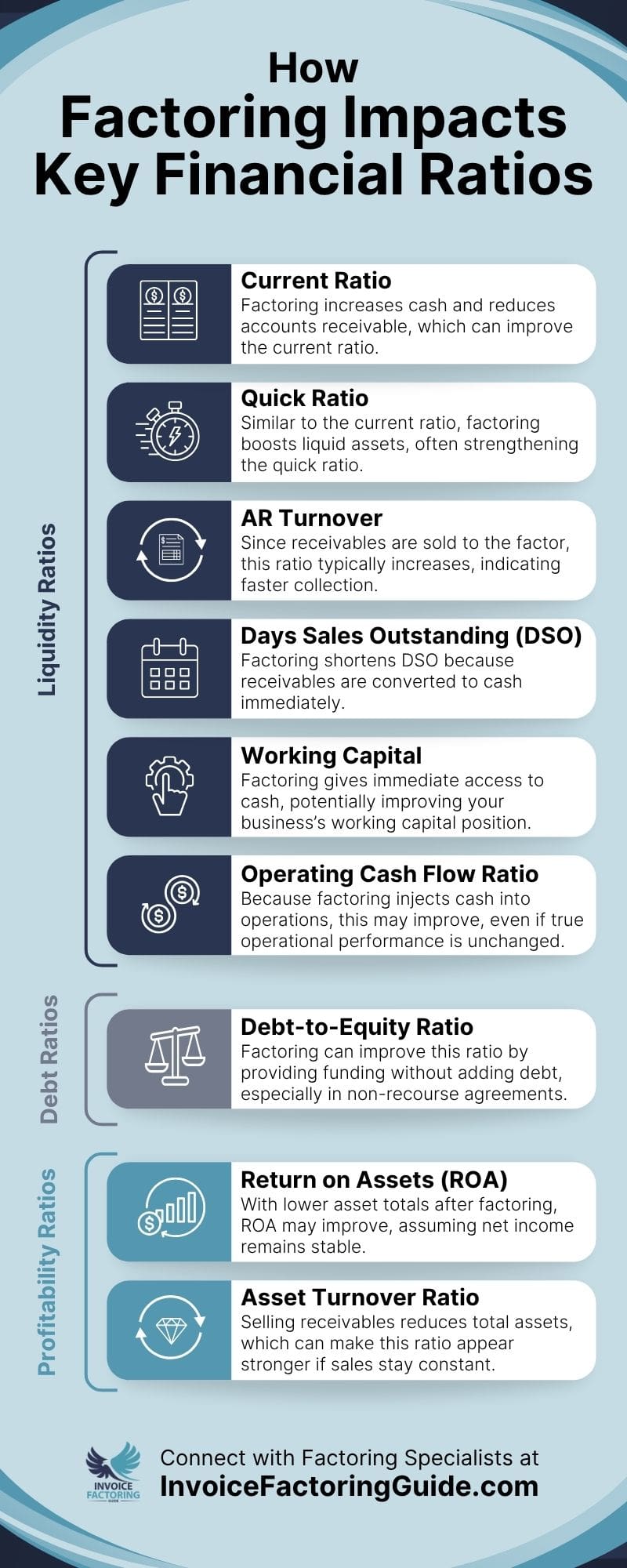

Factoring’s Impact on Liquidity Ratios

Liquidity ratios measure your business’s ability to meet short-term obligations using assets that can quickly be converted to cash. Since factoring accelerates access to cash by turning unpaid invoices into immediate working capital, it typically improves liquidity metrics.

The impact of factoring on liquidity ratios can be especially valuable for businesses operating on thin margins or dealing with long payment cycles. By reducing the lag between billing and collection, factoring gives your business more flexibility to handle day-to-day expenses without relying on credit lines or delaying payments to suppliers. The extent of the impact depends on how heavily your business uses factoring and how frequently your receivables are converted to cash through this method.

Current Ratio

The current ratio is one of the most widely used indicators of short-term financial health. It compares your current assets, like cash, accounts receivable, and inventory, to your current liabilities, or anything due within the next twelve months.

Current Ratio Formula and Calculations

Current Assets ÷ Current Liabilities

A ratio above 1.0 means you have more short-term assets than short-term obligations. For many lenders and partners, this signals that your business is equipped to cover its bills without strain. But the number alone doesn’t tell the whole story. A current ratio of 2.0 may look strong, but if most of your “current” assets are tied up in slow-paying receivables, your actual cash position may be much tighter than it appears.

Factoring and Current Ratios

By converting accounts receivable into cash, factoring can shift the composition of your current assets without changing the total value. Instead of waiting weeks or months for payment, you’re holding cash that can be used immediately. This can help improve your current ratio, or at the very least, strengthen what that ratio reflects. To an outside observer, your business may look more liquid and better positioned to manage its short-term obligations.

This effect is often most noticeable for businesses that carry a high volume of receivables relative to other current assets. The more those receivables are factored, the more the balance sheet reflects actual cash flow rather than delayed income.

Quick Ratio

The quick ratio offers a more conservative view of liquidity than the current ratio. It focuses strictly on assets that can be converted to cash in the short term, excluding inventory and other less liquid holdings.

Quick Ratio Formula and Calculations

(Cash + Accounts Receivable + Marketable Securities) ÷ Current Liabilities

This ratio is commonly used to assess whether a business can meet its immediate obligations without relying on inventory sales or new financing. It is particularly relevant in industries where inventory turnover is slow or unpredictable, and where near-term cash availability matters most.

Factoring and Quick Ratios

By turning accounts receivable into cash, factoring changes the makeup of your liquid assets without altering your liabilities. Even when the total value of your current assets stays the same, shifting a portion of it into cash strengthens the quality of your liquidity. This can lead to an improved quick ratio or enhance the reliability of a stable one.

In financial reviews, this shift is meaningful. Cash is more dependable than receivables, especially when payment terms are long or customer reliability varies. Factoring helps reduce the uncertainty built into this ratio, which makes your short-term financial position appear more resilient to those reviewing your balance sheet.

Current and Quick Ratio Analysis

While each ratio offers value on its own, reviewing them together provides a clearer view of short-term financial strength. The current ratio reflects your total ability to cover immediate obligations using all current assets, including inventory. The quick ratio refines that view by focusing only on assets that are readily accessible. Taken together, they help identify whether a business’s liquidity is supported by actual cash flow or tied up in assets that may be harder to convert when cash is tight.

Accounts Receivable Turnover

The accounts receivable turnover ratio measures how efficiently your business collects payments from customers. It reflects how many times your receivables are converted to cash during a specific period, typically a year.

Accounts Receivable Turnover Formula and Calculations

Net Credit Sales ÷ Average Accounts Receivable

A higher turnover ratio generally indicates strong credit and collection practices. It means your customers are paying on time, and that cash is flowing back into the business at a healthy pace. A lower ratio may suggest delays in collection or issues with customer creditworthiness.

Factoring and Accounts Receivable Turnover

Because factoring accelerates the conversion of receivables into cash, it increases the frequency of collections recorded during a given period. Even though the customer may still take 30 or 60 days to pay, the factoring company pays you up front, so from your perspective, the receivable is cleared much more quickly. The result is a higher turnover ratio that reflects improved cash recovery without changing your credit terms or pressuring your customers.

This shift can strengthen internal cash flow planning and signal improved operational efficiency to external stakeholders reviewing your financial performance.

Days Sales Outstanding (DSO)

DSO calculates the average number of days it takes your business to collect payment after a sale is made. It is closely tied to the accounts receivable turnover ratio but expressed in terms of time rather than frequency.

Days Sales Outstanding Formula and Calculations

(Accounts Receivable ÷ Total Credit Sales) × Number of Days

A lower DSO means you’re collecting faster, which generally signals healthier cash flow. A high DSO can indicate that a large portion of your capital is tied up in unpaid invoices, which limits your ability to reinvest or cover expenses.

Factoring and Days Sales Outstanding

Factoring reduces DSO by providing immediate payment on invoices. Even if your customer still takes thirty or sixty days to pay, your business receives most of the funds up front, effectively shortening the collection period from your perspective. This improves DSO, which can help you track cash efficiency more accurately and present stronger financial metrics in funding conversations.

Working Capital

Working capital is not a ratio, but it is still an important liquidity measure. It reflects the difference between your current assets and current liabilities.

Working Capital Formula and Calculations

Current Assets – Current Liabilities

Positive working capital means your business has enough short-term assets to cover short-term debts. Negative working capital can lead to cash flow challenges and put pressure on day-to-day operations.

Factoring and Working Capital

Factoring helps improve working capital by increasing your available cash without increasing your liabilities. It replaces a less liquid asset, accounts receivable, with immediate funds you can use to pay expenses, manage inventory, or support growth. This can be especially helpful in industries where delayed payments from customers would otherwise limit your ability to operate smoothly.

Operating Cash Flow Ratio

This ratio compares the cash generated from operations to your current liabilities. It answers a key question: can your business cover its short-term debts using cash from normal business activity?

Operating Cash Flow Ratio Formula and Calculations

Operating Cash Flow ÷ Current Liabilities

This ratio differs from others in the liquidity category because it reflects actual cash activity, not balance sheet values. A higher ratio indicates that your core business is producing enough cash to keep up with short-term obligations. A low or inconsistent ratio may suggest reliance on external funding or difficulty maintaining liquidity through operations alone.

Cash Flow Benefits of Factoring

While factoring does not increase operating cash flow in accounting terms, it improves your ability to manage short-term liabilities using cash tied to sales activity. Some businesses use factoring strategically to stabilize this ratio when seasonal fluctuations or long payment terms disrupt the flow of funds.

Factoring’s Impact on Debt Ratios

Debt ratios evaluate how much of your business is financed through liabilities and how that leverage compares to your assets or equity. They offer insight into long-term financial stability, helping lenders and other stakeholders assess the level of risk involved in working with your company.

Because factoring is not considered debt in most cases, it generally has a neutral or positive effect on debt-related metrics. Funds received through factoring are not recorded as loans and do not appear as liabilities on the balance sheet when structured as a true sale. This distinction can improve the appearance of certain ratios and support your business’s credit profile, particularly when compared to more traditional forms of financing.

The degree of impact depends on how the factoring arrangement is structured and how consistently it is used. In non-recourse arrangements, the receivables are fully removed from the balance sheet, offering the most favorable impact. In recourse agreements, or when factoring is treated as a secured borrowing, the effect on debt ratios may be minimal or even neutral.

Debt-to-Equity Ratio

The debt-to-equity ratio compares total liabilities to shareholders’ equity. It is used to evaluate how much financial leverage your business is using and whether your operations are funded primarily through debt or through reinvested earnings

Debt-to-Equity Ratio Formula and Calculations

Total Liabilities ÷ Shareholders’ Equity

A lower ratio typically indicates a more conservative financial structure, which may be viewed favorably by lenders or investors. A higher ratio signals greater reliance on borrowed funds, which could increase perceived risk, especially if earnings are inconsistent or cash flow is tight.

Factoring and Debt Ratios

Factoring generally does not increase this ratio. When structured as non-recourse and treated as a true sale, factoring removes the receivables from the balance sheet without adding to liabilities. The result is a more favorable debt-to-equity ratio, since the business gains access to capital without increasing its debt load.

In cases where factoring is structured with recourse or treated similarly to a loan, the debt-to-equity ratio implications may be less pronounced. However, because factoring is tied to receivables instead of new borrowing, it is often viewed differently than traditional debt.

This distinction helps businesses manage cash needs without increasing leverage on paper. The result is a meaningful difference in debt perception versus cash flow. You gain funding without the liability. Because of this, managing debt ratios with factoring preserves financial flexibility while still supporting growth.

Factoring’s Impact on Profitability Ratios

Profitability ratios assess how efficiently your business generates earnings relative to revenue, assets, or equity. They help you understand whether your operations are yielding sustainable returns and how well resources are being used to support growth.

Factoring does not directly increase profit margins, but it can influence how profitability is expressed in ratio form. By improving cash flow and reducing the need for borrowed capital, factoring may help lower financing costs, stabilize operations, and make better use of existing assets. These effects can lead to stronger performance metrics, even when net income remains unchanged.

The impact is most noticeable in businesses where receivables make up a significant portion of the asset base or where traditional financing would otherwise erode profitability through interest or fees.

Additionally, profitability ratios and factoring may come into play when a business evaluates the financial impacts of factoring. Many businesses have concerns about the impact of factoring fees on profit margins. However, profit trends for factoring clients are usually strong because they’re able to reinvest the money they have already earned in the company much more quickly. If you’re concerned about this aspect, consider calculating factoring costs and including them in your ratios to help predict where you’ll land. Just to remember to also include the opportunities you gain.

Return on Assets (ROA)

Return on assets measures how efficiently your business uses its assets to generate profit. It provides insight into how well your company turns investments in infrastructure, equipment, and receivables into net income.

Return on Assets Formula and Calculations

Net Income ÷ Total Assets

A higher ROA suggests stronger asset efficiency. For capital-intensive businesses, this ratio is often used to track how productively cash, equipment, and receivables are being put to work.

Factoring and Return on Assets

Factoring can influence ROA by altering the size and makeup of the asset base. When receivables are sold to a factor and removed from the balance sheet, total assets decrease. If net income remains steady, this can lead to an improved ROA. Even if the factoring fee slightly reduces profit, the overall ratio may still benefit due to the smaller denominator.

This shift is most relevant in businesses with large receivable balances or low turnover. Factoring helps make those assets productive by turning them into usable cash, which may ultimately strengthen profitability metrics.

Asset Turnover Ratio

The asset turnover ratio measures how efficiently your business uses its total assets to generate revenue. Unlike ROA, which looks at profit, this ratio focuses on top-line sales activity.

Asset Turnover Ratio Formula and Calculations

Net Sales ÷ Average Total Assets

A higher ratio indicates more efficient use of assets in driving revenue. It is often used in performance comparisons across businesses of different sizes, especially in industries where margins vary but asset deployment is a key driver of growth.

Factoring and Asset Turnover Ratio

Factoring affects this ratio by reducing the asset base without impacting reported sales. When accounts receivable are sold, total assets decrease while revenue remains unchanged. As a result, the ratio may improve—even if operational performance is the same.

For businesses that want to demonstrate efficiency to investors or lenders, a stronger asset turnover ratio can support that narrative. Factoring provides a way to unlock working capital while making better use of existing assets, without expanding liabilities or changing sales strategy.

Improve Your Financial Ratios with Factoring

Whether you’re trying to free up capital, keep debt to a minimum, or boost profitability, invoice factoring can help. To explore the fit more or get a complimentary rate quote, talk to a factoring specialist.

FAQs on Factoring and Financial Ratios

What are the most important financial ratios for SMEs?

For small and mid-sized businesses, the most useful ratios often include the current ratio, quick ratio, debt-to-equity ratio, return on assets, and accounts receivable turnover. These metrics help monitor liquidity, leverage, and profitability; key areas that influence funding options, cash flow management, and long-term sustainability.

What are the most important metrics to monitor with factoring?

When using factoring, it’s helpful to track liquidity ratios like current and quick ratios, as well as accounts receivable turnover and DSO. These metrics show how quickly you’re converting invoices to cash and how factoring is supporting your ability to meet short-term obligations without taking on debt.

Should I worry about factoring effects on solvency ratios?

In most cases, no. Factoring is not classified as debt when structured as a true sale, so solvency ratios typically remain unaffected. It may even improve certain metrics by reducing reliance on loans. If you use recourse factoring, check with your accountant to understand how it’s reflected on your balance sheet.

How does invoice factoring affect my company’s financial ratios?

Factoring often improves liquidity ratios by turning receivables into cash without increasing liabilities. It may also enhance efficiency ratios like receivables turnover. When structured as non-recourse, it typically does not impact debt ratios, making it a useful option for improving cash flow without weakening your financial position.

Will factoring make my business look riskier to lenders or investors?

In most cases, no. Factoring is generally seen as a cash flow strategy rather than a sign of financial distress. If it strengthens liquidity or improves collections, it may even enhance your credibility, especially if your balance sheet stays lean and no additional debt is recorded.

Does factoring improve or hurt my current ratio?

Factoring can improve your current ratio by increasing your liquid assets. Since receivables are replaced with cash, your ability to meet short-term obligations improves, without adding new liabilities. The overall effect depends on how frequently you factor and how your assets are structured before funding.

Can factoring mess up my debt-to-equity ratio?

Factoring usually does not harm your debt-to-equity ratio when structured as a true sale. In fact, it may improve the ratio by increasing available funds without increasing liabilities. Only in some recourse arrangements might factoring be treated like debt—check with your accountant to confirm.

What financial statements change when I use factoring?

Your balance sheet and cash flow statement may reflect changes. Accounts receivable are reduced, and cash increases. If structured as non-recourse, there’s typically no new liability recorded. In recourse arrangements, a short-term liability may be added. Your income statement generally remains unchanged, aside from factoring fees.

This article is for educational purposes only and does not constitute business, financial, legal, or tax advice. Speak with a qualified professional about your specific circumstances before making business, financial, legal, or tax decisions.

About Invoice Factoring Guide

Factoring Fee Structures Explained: Breaking Down Your Costs

Factoring Fee Structures Explained: Breaking Down Your Costs The Factoring Payment Process: When and How You Get Paid

The Factoring Payment Process: When and How You Get PaidRelated Insights

Get an instant funding estimate

Results are estimates based on the calculated rate and the total invoice amount provided.

Actual rates may vary.

Request a Factoring Rate Quote

PREFER TO TALK? Call us at 1-844-887-0300

")