Worried you’ll be locked into your factoring contract terms? The good news is that factoring is designed to be flexible, and you have a lot of room to negotiate terms before you sign. Below, we’ll cover some areas of factoring contracts that can potentially limit flexibility and how to address them if the proposed terms don’t work for you.

Factoring Contract Length and Close-Out Terms

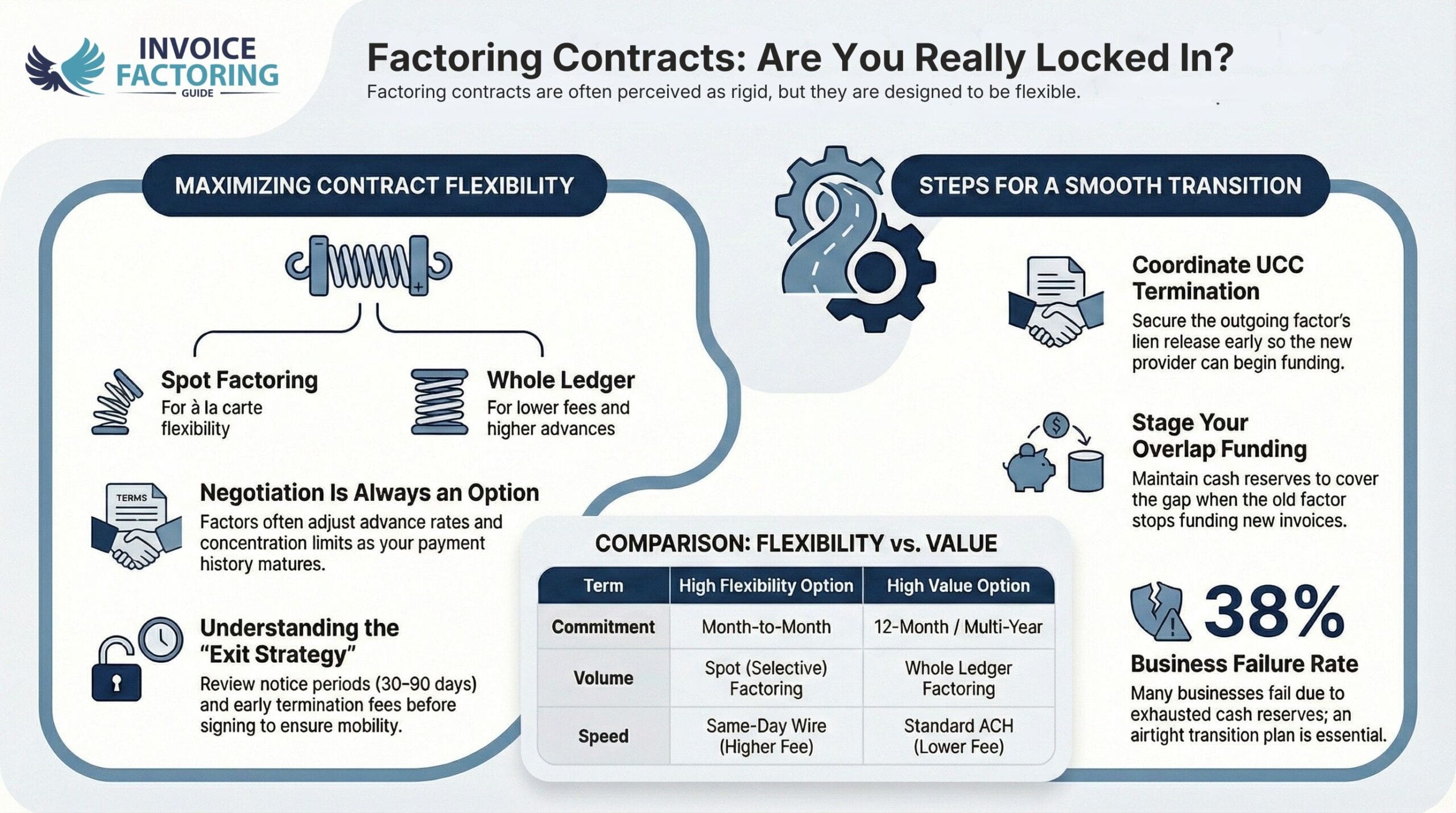

It’s always a good idea to consider your exit strategy before you start factoring. Virtually all businesses stop factoring at some point, often because their cash flow has stabilized. There are a few factoring contract terms to consider that will impact how your departure plays out.

Long-Term vs. Short-Term Factoring Contracts

Many factors offer 12-month or multi-year terms to justify onboarding costs and lock in favorable pricing. A longer commitment often secures lower discount fees, higher advance rates, or waived ancillary charges.

Early Termination Clauses in Factoring

If you decide to exit before the end of the term, the agreement may call for liquidated-damages fees or repayment of waived costs. These clauses are intended to discourage abrupt departures, but can often be negotiated down if your volume or tenure is strong.

Contract Exit Fees

Separate from early termination language, some agreements list flat close-out fees that cover final reconciliations and administrative work. Understanding these charges up front helps you weigh whether a shorter contract plus higher recurring fees or a longer contract with a predictable exit fee delivers the best overall value.

Auto-Renewal

Contracts sometimes renew automatically for successive periods unless either party gives written notice. Auto-renewal maintains continuous funding and relationship perks. However, you’ll want to mark your calendar so you can revisit pricing or explore alternatives before the renewal date.

Notice Periods

Factors typically require 30 to 90 days’ written notice to wind down the account, verify ledger balances, and release reserves. Once notice is submitted, you generally cannot submit new invoices, so plan timing carefully to avoid unexpected cash flow gaps.

Volume Commitments

Another major area that impacts flexibility is which invoices you factor. Some contracts specify which invoices you need to factor or have minimum volumes. While these rules are not inherently bad because they do typically result in better terms, you also want to ensure you’re not over-committing and factoring invoices when the funds won’t directly improve your ability to operate and generate profit.

Whole Ledger Factoring

With whole ledger factoring, you agree to factor every qualifying invoice during the contract term, giving the factor full visibility of your receivables and letting them spread risk across the entire book. In return, you often receive lower discount fees, higher advance percentages, and faster reserve releases. This approach works well when sales are steady and you prefer one simple, predictable funding channel.

Spot Factoring

With spot factoring, also known as single-invoice factoring or selective factoring, you choose invoices à la carte, funding only when cash gaps appear. Spot arrangements maximize flexibility and suit seasonal businesses or companies testing new customers. Expect higher per-invoice fees, more stringent credit reviews, and occasionally lower advance rates because the factor cannot count on consistent volume.

Minimum Monthly Volume Requirements

Contracts may state a dollar amount or a percentage of sales that must be factored each month. Hitting these targets keeps pricing intact, while falling short can trigger make-up fees that offset the factor’s idle capital costs.

Note that some providers let clients lock in tiered pricing where better rates kick in once a certain funded-volume threshold is reached. This bridges the gap between full commitment and pure spot usage, rewarding growth without forcing every invoice through the program.

Payment Amounts and Timelines

Quick access to funds is the heart of factoring, yet payment amounts and timing can vary by agreement. Clarify these details up front so your cash flow rhythm aligns with your needs.

Advance and Reserve Rates

The factoring advance is the portion of the invoice you receive upfront. The reserve, also called a hold-back, is the portion that’s retained until after your client pays their invoice. Factors typically set a headline percentage tailored to your industry, customer mix, and historic dilution to give you a predictable working-capital benchmark. However, you may be able to negotiate higher advance rates at a higher cost or save by allowing for greater reserves. Some factors will also let you have different advance rates for different customers.

Disbursement Speed Options

Many factors default to Automated Clearing House (ACH) transfers with a standard two-day turnaround, while offering same-day wire funding for an added fee. Confirm whether you may choose the faster option only when you need it, or if you must commit at signing, then weigh occasional wire costs against the convenience of on-demand speed.

Reserve Release Schedule

Contracts typically outline when the held-back balance is released after a debtor pays. This sometimes happens immediately upon clearance, but may also occur on a set reconciliation date. Ask whether the schedule can be adjusted as volume grows or customer payment patterns change. You may be able to accelerate the pace of your reserve release as the risk for the factor decreases.

Additional Terms That Impact Contract Flexibility in Invoice Factoring

Beyond contract length and volume, a handful of factoring contract clauses determine how smoothly you can pivot as sales patterns or customer mixes evolve. Review the following items with your factor so the agreement supports both cash flow stability and growth.

Credit Approval Controls

Eight percent of B2B invoices are written off as bad debt, and half are not paid on time, according to Atradius. Because of this, most factors retain the right to review and approve each debtor before funding an invoice. This oversight shields your business from slow-paying or high-risk accounts and may unlock credit-insurance pricing advantages. However, be sure the factor’s rating criteria align with your sales strategy so promising new customers can flow through the program without delay.

Maximum Concentration Limits

Agreements frequently cap the percentage of total receivables that can come from a single customer or industry segment. These limits diversify risk and preserve advance rates, yet they can require partial funding when one client represents a large share of revenue. If you rely on key accounts, negotiate higher thresholds or carve-out exceptions to keep working capital levels predictable.

Steps to Take When Breaking a Factoring Contract or Switching Factoring Providers

If you’re already locked into a factoring contract that doesn’t work for you, and you can’t negotiate new terms, you can terminate your agreement. To ensure the smoothest transition possible, address the points outlined below.

Verify Notice Requirements

Review the contract for written notice rules so you can time the request and pause new invoice submissions appropriately.

Calculate Exit and Make-Up Fees

Add any early-termination charges and minimum-volume shortfall costs to understand the true price of leaving.

Coordinate Reserve Release Timing

Confirm when outstanding reserves and chargeback balances will clear so working capital remains steady during the transition.

Arrange UCC Termination or Assignment

Secure the outgoing factor’s release of its Uniform Commercial Code filing early, allowing the new provider to perfect its own lien without delay.

Align Debtor Notifications

Decide which party will advise customers of new payment instructions to prevent misapplied funds and preserve relationships.

Stage Overlap Funding

There will be a brief period when the current factor completes collections, and you cannot submit new invoices. Ensure you have adequate funding during this period. Bear in mind that 38 percent of businesses fail because they’ve exhausted their cash reserves or couldn’t secure funding, per Forbes. It’s essential to have an airtight plan.

Prepare Clean Ledger and Aging Reports

Up-to-date reporting speeds the new factor’s due diligence review and helps lock in favorable advance rates.

Evaluate Added Value

Compare service levels, such as faster payments or sector expertise, to be sure the benefits of switching outweigh transition costs.

Leverage Negotiation Opportunities

The process of exploring alternatives often opens discussions to improve fees, advance rates, or reserve schedules, whether you stay or move.

Get Factoring Contract Terms That Work for You

Now that you know what to look for in your factoring agreement, the next step is finding out what terms you qualify for. To get started or talk to a factoring specialist, request a complimentary rate quote.

FAQs on Factoring Contract Terms and Factoring Agreement Flexibility

How do I get out of a factoring contract?

Start by reviewing the notice clause, which usually requires 30 to 90 days’ written notice and suspension of new invoice submissions. Calculate early-termination and close-out fees, then schedule the change so reserves are released when expected. Coordinating lien releases and customer notifications keeps cash moving while you transition funding.

What do I do if my factoring contract terms no longer work for me?

Begin with an open conversation with your account manager. Share updated sales forecasts or customer shifts and request adjustments to advance rates, concentration limits, or reserve schedules. Established performance often earns concessions. If revisions are unavailable, compare exit costs with the benefits of switching to a factoring provider whose terms match your current needs.

Can I renegotiate my factoring contract after it has been signed?

Yes. Factors regularly revisit pricing and structure as relationships mature. Demonstrating prompt payments, higher invoice volume, or stronger debtor credit can justify improved discount fees, quicker reserve releases, or greater advance percentages. Approach renegotiation well before renewal dates, present clear performance data, and outline projected growth to secure favorable adjustments.

About Invoice Factoring Guide

How to Use Factoring for Financial Stability and Overcome Uncertainty

How to Use Factoring for Financial Stability and Overcome UncertaintyRelated Insights

Get an instant funding estimate

Results are estimates based on the calculated rate and the total invoice amount provided.

Actual rates may vary.

Request a Factoring Rate Quote

PREFER TO TALK? Call us at 1-844-887-0300

")