Five percent of B2B invoices in the U.S. are written off as bad debt, according to the latest from Atradius. While that may not seem like much, every dollar that’s earned that does not come back to the company can create challenges, especially for small and mid-sized businesses. In this guide, we’ll explore the causes of bad debt, how factoring can reduce bad debt, and additional steps you can take to eliminate it.

Common Causes of SME Bad Debt

Bad debt can creep up on any business, but small and mid-sized enterprises (SMEs) tend to feel the effects more sharply. A few slow-paying or defaulting customers can throw off your entire cash flow strategy. Understanding where bad debt begins is the first step in preventing it.

Loose Credit Policies

Extending credit without clear terms or adequate vetting often leads to unpaid invoices. Many SMEs prioritize growth and customer relationships, but skipping credit checks can put your business at risk.

Economic Downturns

When inflation rises or demand dips, even reliable customers may struggle to pay on time. During these periods, delinquency rates climb across nearly every industry.

Overreliance on a Few Customers

Depending heavily on one or two key clients can create vulnerability. If a major customer delays payment or folds, the loss can ripple through your entire operation.

Inefficient Collections Processes

Without a consistent follow-up system, invoices slip through the cracks. Late reminders, poor communication, or unclear escalation procedures all contribute to higher write-offs.

Industry-Specific Risks

Some sectors, such as construction, logistics, and manufacturing, naturally face longer payment cycles and higher default rates. These timelines can leave your business financing customer debt longer than intended.

The Impact of Bad Debt on Your Business

Bad debt affects how you plan, spend, and grow. When unpaid invoices pile up, your financial foundation starts to shift in ways that can quietly undermine your long-term goals.

Cash Flow Disruptions

Cash that should be flowing in gets locked up in overdue invoices. This forces you to delay your own payments, dip into reserves, or take on high-interest debt to cover everyday costs.

Reduced Working Capital

Less working capital means fewer resources for payroll, inventory, or marketing. Even small fluctuations in cash flow can make it difficult to seize growth opportunities or handle unexpected expenses.

Strained Vendor Relationships

When your customers pay late, it can cause a domino effect. You may struggle to pay your own suppliers on time, damaging relationships or resulting in stricter payment terms.

Weakened Financial Health

Unpaid invoices inflate accounts receivable, which can distort your balance sheet and make it harder to secure financing. Lenders and investors often see high receivables as a warning sign of poor cash management.

Operational Distraction

Chasing payments takes time away from revenue-generating activities. Teams that should focus on growth or customer service end up spending hours following up on overdue accounts.

How Factoring Works

Before we get into using factoring for bad debt reduction, let’s take a quick look at how it works.

Most businesses use factoring for cash flow acceleration. Instead of waiting weeks or months for customer payment, your business sells its accounts receivable to a factoring company at a small discount. The factor advances most of the invoice value right away, then takes on the responsibility of collecting payment from your customers.

This makes it distinct from other forms of business funding and much more accessible than traditional forms of financing like business loans or lines of credit. In fact, you can qualify for factoring even if you’ve been denied by banks. Getting approved for factoring is fast and easy, regardless of your years in business or credit score.

Overview of the Factoring Process

Factoring may sound complex, but the process is straightforward once you understand the steps involved.

- Submit Invoices: You provide the factoring company with invoices for completed work or delivered goods.

- Verification and Approval: The factor verifies that the invoices are valid and that your customers have a reliable payment history.

- Receive Immediate Funds: You receive an advance, often between 80 and 90 percent of the invoice value, within one or two business days. Some factors even provide same-day payments.

- Customer Payment: Your customer pays the factoring company according to the invoice terms.

- Balance Release: Once the customer pays in full, the factor releases the remaining balance, minus a small fee for the service.

Types of Factoring

Different types of factoring offer varying levels of control and protection. The right option depends on your risk tolerance, industry, and customer base.

- Recourse Factoring: You remain responsible if a customer fails to pay. This option usually comes with lower fees because the factor’s risk is minimal.

- Non-Recourse Factoring: With non-recourse factoring, the factor assumes the risk of non-payment. This provides greater protection for your business, but at a slightly higher cost.

- Spot Factoring: With spot factoring, you choose which invoices to factor rather than committing your entire receivables portfolio. This is ideal for businesses that want flexibility.

- Contract Factoring: You agree to factor all or a large portion of your invoices on an ongoing basis, often resulting in lower overall rates.

Key Factoring Benefits

Factoring strengthens your financial resilience and gives you the confidence to grow without fear of unpaid invoices.

- Improved Cash Flow Predictability: Steady cash flow allows you to budget accurately and reinvest in operations without delay.

- Operational Efficiency: Outsourcing collections frees your team to focus on revenue-generating tasks rather than chasing late payments.

- Financial Freedom: You can use your working capital from factoring in whatever way makes the most sense for your business. Many leverage factoring for core operations, while others use it to help cover major purchases and fund growth activities.

- Scalability: As your sales grow, so does your access to working capital since funding is tied to your receivables, not your credit history.

- Reduced Bad Debt Exposure: When factoring is used strategically, it acts as a financial safety net that shields your business from customer insolvencies. We’ll explore this more in just a moment.

Additional Factoring Company Benefits

In addition to the general benefits of factoring, some factoring companies offer additional services that can help your business grow.

- Invoice Preparation: While collections services are standard, some factors will also prepare invoices on behalf of your business to save you even more time.

- Additional Funding Options: When factoring isn’t the right fit, some factors can also provide you with asset-based loans, commercial credit cards, equipment leasing and financing, insurance premium financing, and more.

- Industry-Specific Perks: If you work with a factoring company that specializes in your industry, you may be able to access additional benefits. For instance, trucking factoring companies may offer load board access, fuel advances, fuel discount cards, roadside assistance programs, and tire discount programs.

How Factoring Can Help Reduce Bad Debt

Now that you’ve seen how factoring works and some of the key benefits, let’s dig into how it can help you reduce bad debt.

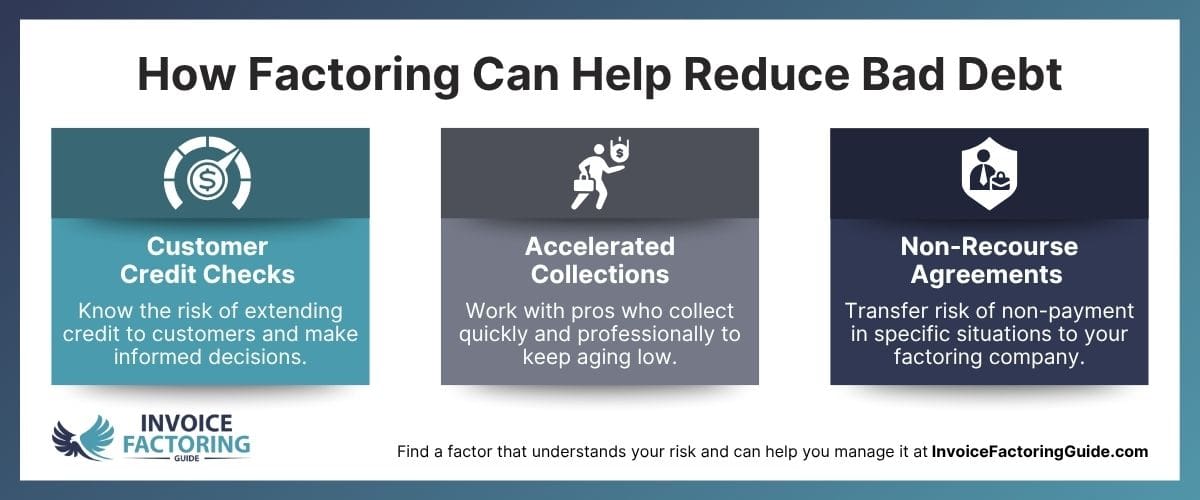

Customer Credit Checks

Almost every instance of bad debt begins with a credit risk that slipped through unnoticed. Factoring companies address this head-on through customer credit evaluations.

When you work with a factoring company, their credit team assesses each customer before approving an invoice for funding. They use industry databases, payment histories, and financial reports to determine who is reliable and who might pose a risk.

- Proactive Risk Assessment: Analyze your customers’ payment behavior before extending credit, helping you avoid potential write-offs.

- Data-Driven Decisions: Access to up-to-date credit data ensures your approval process goes beyond instinct or limited internal information.

- Ongoing Monitoring: Factors continuously track customer payment activity, alerting you if a client’s financial condition worsens.

This built-in credit protection gives you the confidence to extend terms to strong customers while identifying those who could threaten your profitability. In essence, you gain a dedicated credit department without the added payroll expense.

Accelerated Collections

The longer an invoice remains unpaid, the less likely you are to be able to collect at all. In fact, just 18 percent of invoices are paid after 90 days, Entrepreneur reports.

Factoring companies help stop the clock before it gets that far. Collections are part of their core business operations. They specialize in getting invoices paid quickly, efficiently, and with professionalism.

- Expert Collection Practices: Factoring teams use proven methods and up-to-date technology to follow up on payments promptly, ensuring no invoice slips through the cracks.

- Positive Customer Experience: Communication is handled courteously and consistently, preserving your relationships while still prioritizing timely payment.

- Higher Recovery Rates: Because factors collect every day, they maintain strong relationships with payers and understand how to navigate internal systems to resolve delays.

In other words, factoring companies know how to get money in the door and do it in a way that reflects well on your business.

Non-Recourse Agreements

Non-recourse factoring offers another layer of protection by shifting the risk of customer non-payment to the factoring company.

- Risk Transfer: If a customer goes out of business or fails to pay due to insolvency, the factor absorbs the loss instead of your company.

- Stronger Financial Security: This arrangement prevents one client’s financial failure from disrupting your entire operation.

- Peace of Mind: You can extend credit with greater confidence, knowing your receivables are backed by a partner committed to mitigating risk.

As mentioned earlier, this type of agreement typically carries slightly higher fees than recourse factoring. However, for many businesses, the added security far outweighs the cost, especially in industries prone to late or missed payments.

Additional Tips for Managing Non-Paying Customers

Factoring goes a long way toward reducing bad debt, but it should be part of a broader credit management strategy. Strong internal practices ensure that even the most reliable customers stay on track with payments.

Have Clear Credit Policies

Set defined payment terms and communicate them early. Make sure customers understand when payments are due and what happens if they fall behind.

Invoice Consistently

Send invoices immediately after goods are delivered or services are completed. Accuracy and timing signal professionalism and reduce disputes.

Review Accounts Regularly

Monitor aging reports to identify slow payers early. Revisit payment terms with customers who consistently fall behind and consider adjusting their limits.

Develop Defined Escalation Steps

Outline your collection process in advance. For example, send a friendly reminder at 30 days, a firmer notice at 60 days, and consider outside assistance after 90.

Build Strong Customer Relationships

Stay in touch with customers beyond billing. Open communication often prevents payment delays caused by misunderstandings or administrative issues.

Get Started Reducing Bad Debt with Factoring

Whether you simply want to accelerate cash flow or are looking for innovative ways to eliminate bad debt, factoring can help. To be matched with a factoring company that understands your industry and its unique risks, request a complimentary rate quote.

FAQs About Bad Debt in Businesses

When choosing factoring services, should I go with recourse or non-recourse to avoid bad debt?

Non-recourse factoring provides more protection from bad debt because the factoring company assumes the risk of customer non-payment due to insolvency. Recourse factoring, on the other hand, places that responsibility back on your business. The right choice depends on your customers’ reliability and how much risk you’re willing to carry.

Do factoring and working capital loans both help reduce bad debt?

Factoring helps reduce bad debt by preventing it through credit screening, professional collections, and, in some cases, risk transfer. Working capital loans improve liquidity but do not protect against non-paying customers. Factoring strengthens both cash flow and credit control, while loans only address cash shortages after payment issues arise.

What’s the factoring cost comparison between recourse and non-recourse agreements?

Recourse factoring typically costs less because you retain responsibility if a customer fails to pay. Non-recourse factoring includes added protection against bad debt, so fees are slightly higher to offset the factor’s risk. The difference is often marginal compared to the security gained through non-recourse coverage.

Who is responsible for bad debts in recourse factoring?

In recourse factoring, your business remains responsible if a customer fails to pay. The factoring company advances funds based on the invoice value but can reclaim those funds if the customer defaults. This option offers lower fees but requires you to manage more credit risk internally.

Who is responsible for bad debts in non-recourse factoring?

In non-recourse factoring, the factoring company assumes responsibility for losses if a customer becomes insolvent or files for bankruptcy. Your business is protected from that specific form of bad debt, allowing you to extend credit more confidently without fearing a total loss from customer non-payment.

How does invoice factoring reduce the risk of bad debt?

Invoice factoring reduces bad debt risk by screening your customers’ credit before invoices are funded and managing collections professionally. This ensures you only extend terms to financially stable buyers and receive payment faster, protecting your business from defaults and minimizing unpaid receivables.

Can factoring eliminate bad debt completely?

Factoring cannot eliminate bad debt entirely, but it significantly reduces the risk. Through credit checks, structured collections, and non-recourse options, factoring limits exposure to unpaid invoices. You still need sound credit practices, but factoring adds a financial safety net that prevents most payment losses.

Does factoring protect against customers who go bankrupt?

In non-recourse factoring, the factoring company absorbs losses if your customer becomes insolvent or files for bankruptcy. This protection prevents your business from carrying the financial burden of customer failures, making it an effective safeguard against the most severe types of bad debt.

Is factoring better than credit insurance for preventing bad debt?

Factoring and credit insurance both protect against bad debt, but factoring adds the benefit of immediate cash flow and professional collections. With factoring, you receive funds upfront and transfer much of the risk to the factor, while credit insurance only reimburses you after a loss.

What types of businesses use factoring to manage bad debt?

Industries with long payment cycles or high invoice volumes, such as trucking, manufacturing, staffing, and wholesale, often use factoring to control bad debt. These sectors face a greater risk of late or missed payments, and factoring offers both consistent cash flow and built-in credit protection.

Can factoring help businesses with existing bad debt?

Factoring does not erase existing bad debt, but it helps prevent new losses from forming. Once unpaid invoices become uncollectible, factors cannot fund them. However, moving forward with factoring strengthens cash flow and reduces the chance of future write-offs through better credit management and professional collections.

About Invoice Factoring Guide

Factoring Exit Strategies: A Comprehensive Guide to Transitioning Away from Factoring

Factoring Exit Strategies: A Comprehensive Guide to Transitioning Away from Factoring How Factoring Improves Liquidity

How Factoring Improves LiquidityRelated Insights

Get an instant funding estimate

Results are estimates based on the calculated rate and the total invoice amount provided.

Actual rates may vary.

Request a Factoring Rate Quote

PREFER TO TALK? Call us at 1-844-887-0300

")